Can I Register a Car With a Insurance Binder

Key Takeaways

- An insurance binder is temporary evidence of insurance coverage.

- It is not an insurance policy or a certificate of insurance.

- A valid binder must include key policy details and the signature of an authorized issuer.

Questions

- My lender is asking for an insurance binder. Where do I get one?

- How long does it take to get one?

- What does an insurance binder actually mean?

When the car dealer asks you for an insurance binder, don't panic. The dealer's not expecting you to pull out a three-ring notebook stuffed with policy documentation. It is not a filing system — it's an official document that verifies your coverage.

What is an insurance binder?

An insurance binder is a short document that verifies your insurance coverage before your policy is issued. When you apply for and purchase insurance, the insurer doesn't generate your policy documentation immediately. There's a processing lag — usually 10 to 30 days — while the insurer verifies your information and documents your coverage internally. At that time, you're likely to need proof of insurance, and that's where the binder comes in. Insurers issue these binders immediately and stand in as evidence of coverage until you receive your full policy documentation.

All types of insurance issue binders — car, motorcycle, home, boat insurance, business insurance, and even livestock insurance.

Definition of an insurance binder

Technically, a binder is a legal contract. The binder functions as proof of your coverage if you need to file a claim before your policy is issued. For that reason, it must outline the key terms, such as named insurers, coverages, and deductibles. The insurance representative's contact info must be listed on the document. Also, the binder's effective date and expiration date. The binder must also be issued and signed by an authorized insurance representative.

When you need an insurance binder

Whenever required to carry insurance, you'll need an insurance binder. When you finance a car, for example, the lender requires you to insure that car — because it's used as collateral for your loan. The car dealer will ask you to present a binder when you buy the car, or soon thereafter. The same applies to a home you're mortgaging — your lender will require you to bring an insurance binder to your home's closing.

Car and home lenders commonly require binders, but there are many more situations you might need one. See the table below for additional examples.

Insurance Binder Request Reasons by Line of Business

| Type of binder | Requested by | Reason for binder request |

| Car | Car loan lender | The car is used as collateral for your car loan. As such, the lender has an interest in protecting that car's value, and your ability to repay the loan. Liability, collision, and comprehensive coverages support those interests. |

| Homeowners | Mortgage lender | The home is used as collateral for your mortgage. As with a car loan, your mortgage lender requires the insurance as a way to protect the collateral's value, and your ability to repay the loan. |

| Title | Mortgage lender | If there are defects on the property's title, they could impact the lender's ability to foreclose if you don't make your mortgage payments. Title insurance protects you and the lender against those defects. |

| RV | Lender or renter | If you buy an RV, the insurance binder works just as a car binder would — protecting the lender against damage to the collateral. If you rent an RV, the rental company will require a binder as proof of coverage, before you drive away. |

| Commercial property | Landlord | When you rent commercial property, your landlord will require you to carry insurance. You'd normally need coverage on your portion of the building, along with coverage on your inventory and assets in the building. The landlord will require you to present the binder as proof of coverage before you move in. |

Even if you're not required to present an insurance binder to a lender or landlord, you should request the binder anytime you initiate coverage on anything. That may sound dramatic, but it's the right approach. Here's why. There's a reason you're buying insurance, and that's to protect yourself from some type of loss. If something bad does happen, like you wreck your new car, you'll want that binder on hand to resolve matters quickly.

What information does an insurance binder include?

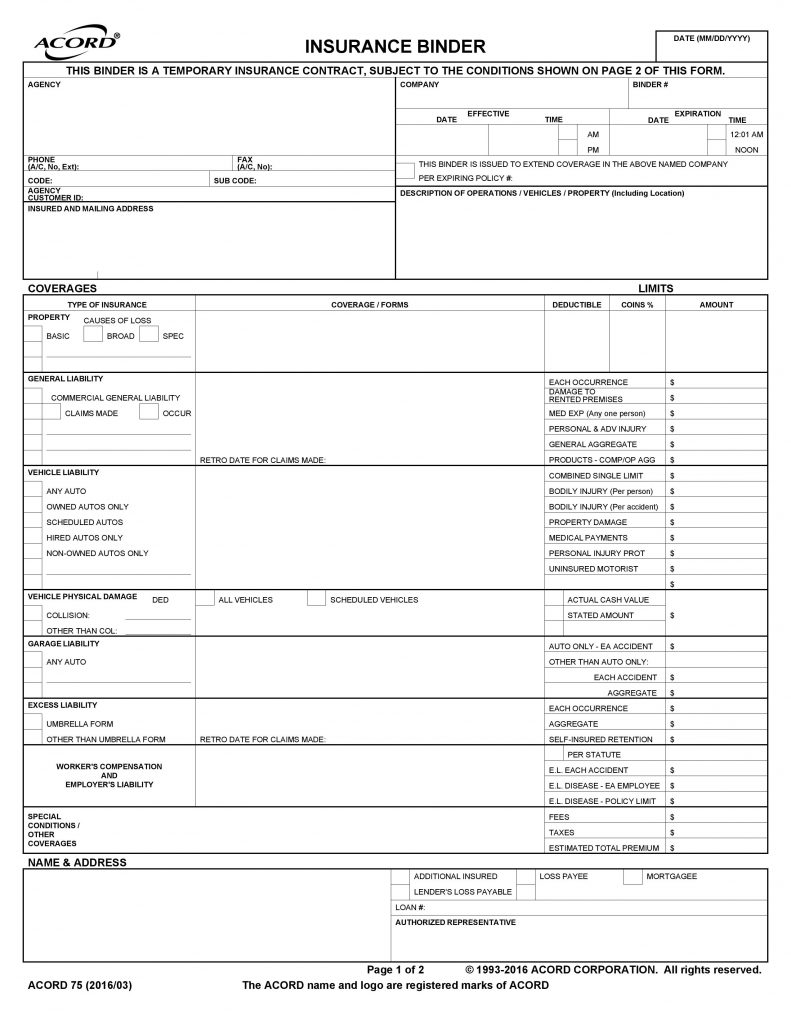

Because insurance binders are legal documents, they must adhere to state insurance law. For that reason, you won't see a handwritten note or an email that's intended to serve as a binder. Instead, you will see an official-looking document and it's most likely a form known as Acord 75. Acord 75 is widely used by insurers nationwide because it's designed to contain all the essential information, including state-specific legal language. Acord 75 serves as evidence for property insurance, general liability insurance, vehicle liability insurance, vehicle physical damage insurance (like collision), garage liability, excess liability, worker's compensation and employer's liability insurance.

A valid binder must include:

- The name and contact information of the insurance representative.

- The name and contact information of the insured — that's you.

- The binder's effective date and expiration date. Insurers like to be specific about this, so you'll usually see an effective time and expiration time also.

- Description of the insured property. e.g. the car, motorcycle, home, RV, commercial property, etc.

- The type of insurance, coverage levels, deductibles, and coinsurance.

- A retroactive date that applies to claims, if applicable.

- Legal language such as, "subject to policy conditions and exclusions." This means the binder adheres to the terms of your policy. Your homeowners insurance, for example, may specifically exclude a shed located on your property. The coverage referenced in the binder would then also exclude the shed.

- A signature of the insurance representative.

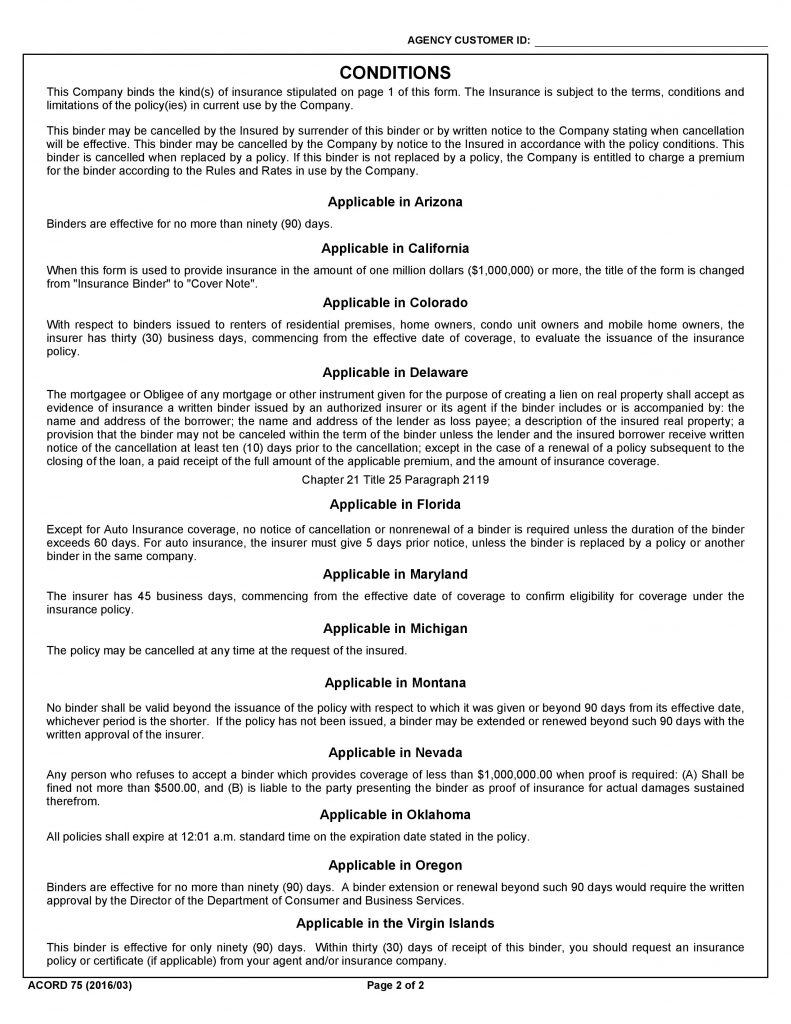

- State-specific conditions. Some states legally define maximum or minimum binder terms. In Arizona, for example, a binder cannot be effective for more than 90 days. This is preprinted on Page 2 of Acord 75 and would override the binder effective dates on the front.

Insurance binder vs. insurance policy

The binder documents your coverage, but so does an insurance policy and a certificate of insurance. So, are these documents all really the same thing? In a word, no. A binder is not interchangeable with a policy or certificate of insurance. The difference is mostly about timing. Binders are only valid for a short time period, such as 30 days. And, they're only issued when the insurance policy doesn't exist yet. Once the actual policy is issued, that policy replaces the binder, voiding it.

Note that a binder is not a guarantee that the policy will be issued — it's more like a handshake that the insurer intends to issue a policy. The insurer must cover you until the binder's stated expiration, and also will collect premiums for that period of time. But if a policy is not issued, for whatever reason, you would not have coverage once the binder expires. Although the insurer must notify you in advance if no policy is being issued, it's wise to keep track of your binder's expiration date. If you haven't received a policy within a week prior to expiration, follow up with your insurance representative.

How to get an insurance binder

Binders are as easy to get as insurance. When your insurer agrees to the coverage, you can request and receive a binder within a day or two. The hardest part is providing the information required for your insurance application, along with form of payment. Once complete, the insurer should issue the binder and email it to you. You can then print it out and keep it with you as proof of coverage.

Manage your insurance binders

It's natural to fulfill a lender's request for a binder, and then promptly forget all about it. Most of the time, that approach will work out. The insurance company should stay on top of the process and send your policy by mail within 10 days. But things do slip through the cracks. In a worst-case scenario, your coverage lapses and you are unknowingly driving around town without insurance.

Avoid that outcome by staying organized — perhaps even with a three-ring notebook. Make a note of your binder's expiration date and stay in close contact with your insurance rep until you receive that policy.

Can I Register a Car With a Insurance Binder

Source: https://honestpolicy.com/learn/insurance-binder-everything-you-need-to-know/

0 Response to "Can I Register a Car With a Insurance Binder"

Post a Comment